Your Guide to Singapore’s Wage Credit Scheme

By Joffre Breininger

By Joffre Breininger

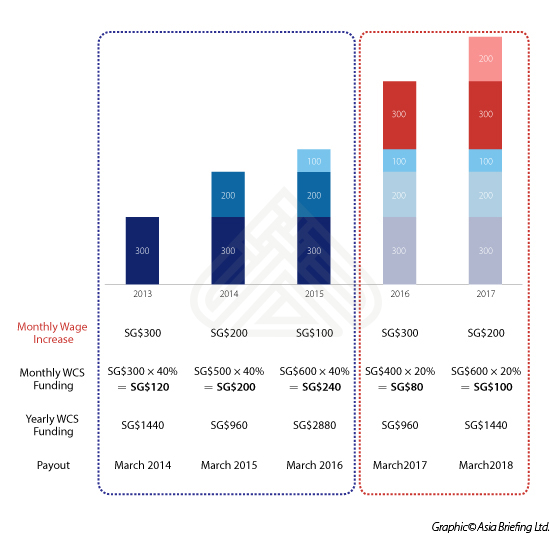

To help companies compensate rising wage costs, the Singaporean government introduced the Wage Credit Scheme (WCS) in 2013, co-funding 40 percent of wage increases. Originally set to expire in 2015, the government announced in its recent 2015 Budget that the measure would be prolonged until year of assessment (YA) 2017, although at half the rate of the current subsidy. In this second tranche, for any hike in salary granted in YA 2015 and sustained throughout 2016 and 2017, employers will still be granted a support of 20 percent for the two additional years.

RELATED: Understanding how Singapore’s Budget 2015 will Affect your Business

RELATED: Understanding how Singapore’s Budget 2015 will Affect your Business

So far, this measure has been fruitful: employees in Singapore can expect a higher salary in 2015, according to the 2015 Salary Guide from British human resources and recruiting firm Hays. The study predicts that around 94 percent of all employees in the city-state will look forward to receiving increased wages, a general trend in the last few years.

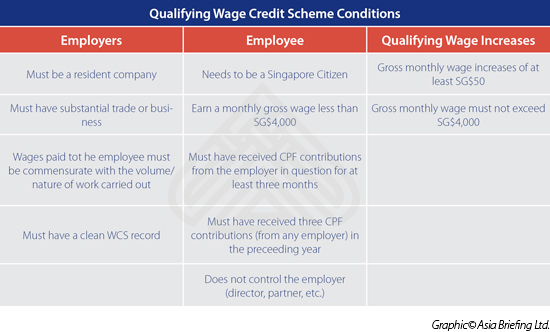

How to Qualify for the Wage Credit Scheme

All employers are eligible for the Wage Credit Scheme – as long as they are a resident company with substantial business in Singapore and employ Singapore Citizens. Furthermore, they need to have contributed to their Central Provident Fund (CPF) for at least three months in the qualifying year.

Employees need to earn a gross monthly salary of less than SG$4,000 and the minimum gross monthly salary increase for the qualifying year must be at least SG$50. In cases where due to a salary hike the threshold is exceeded, only the portion below SG$4,000 will be funded.

Through various additional conditions the Inland Revenue Authority of Singapore (IRAS) aims to minimize attempts of abuse: Wage increases are assessed on an individual basis, and sometimes IRAS will request supporting documents for the purpose of verification. If employees did not carry out substantial work, the wage increase for a certain period of time is out of proportion or the employer provided false or misleading information, they will be disqualified from the measure.

It is important to note that, although employers also have to contribute to Permanent Residents’ CPF, they do not qualify as employees eligible for the Wage Credit.

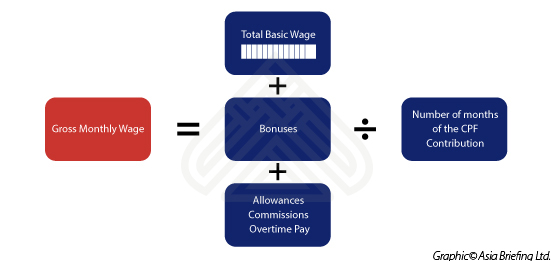

How to Calculate the Wage Credit

For example, a company which hired a new employee in January 2012 who received a gross monthly wage increase of SG$300 in 2013, SG$200 in 2014 and SG$100 in 2015. For 2015, the employee’s monthly government co-funding would be SG$240 – which translates to SG$2880 per year, since it also includes the incremental wage increase granted in the two previous years. The 40 percent Wage Credit for 2015 is computed not only based on the SG$100 salary hike of 2015, but on SG$600, including the SG$300 and SG$200 wage raises from 2013 and 2014, respectively.

Accrued wage increases from 2013 and 2014 will not be subsidized during the Wage Credit Scheme extension (2016/2017), while wage increases granted in 2015 can be included in future calculations.

The Wage Credit Scheme allows companies to free up resources in order to make investments and help the company grow. Employers should seize the opportunity and increase their workers’ salaries while the scheme still subsidizes the hike.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email asean@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam in order to effectively manage and strategically plan their Vietnam operations.

The 2015 Asia Tax Comparator

In this issue, we compare and contrast the most relevant tax laws applicable for businesses with a presence in Asia. We analyze the different tax rates of 13 jurisdictions in the region, including India, China, Hong Kong, and the 10 member states of ASEAN. We also take a look at some of the most important compliance issues that businesses should be aware of, and conclude by discussing some of the most important tax and finance concerns companies will face when entering Asia.

The Asia Sourcing Guide 2015

The Asia Sourcing Guide 2015

In this issue of Asia Briefing, we explain how and why the Asian sourcing market is changing, compare wage overheads, and look at where certain types of products are being manufactured and exported. We discuss the impact of ASEAN’s Free Trade Agreements with China and India, and highlight the options available for establishing a sourcing model in three locations: Vietnam, China, and India. Finally, we examines the differences in quality control in each of these markets.

- Previous Article The Cost of Business in Cambodia Compared With China

- Next Article The Cost of Business in Malaysia Compared With China