ASEAN & the Eurasian Economic Union. Room For Growth in Bilateral Trade & Supply Chain Developments

Op/Ed by Chris Devonshire-Ellis

ASEAN’s trade is largely taken up with other countries in Southeast Asia, China, and India; however, that environment is beginning to change with the addition of bilateral trade and services with the Eurasian Economic Union, and with Russia especially.

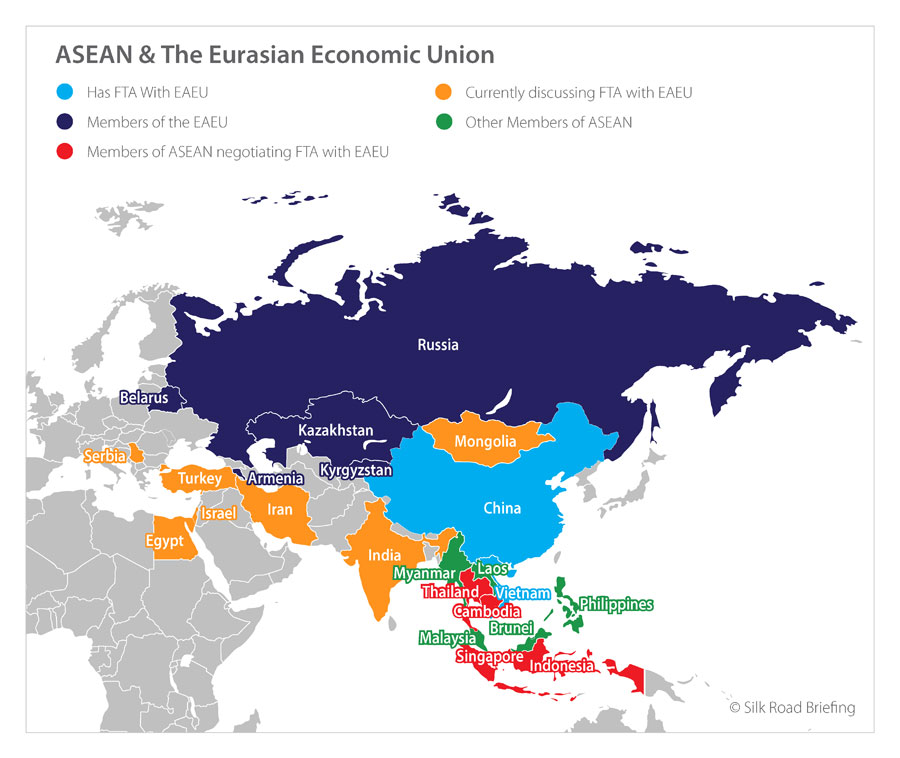

The Eurasian Economic Union (EAEU) is a trade bloc that includes Armenia, Belarus, Kazakhstan, Kyrgyzstan, and Russia. While that appears an eclectic group, is has huge geopolitical and trade potential significance as it essentially extends from the borders of the EU to the borders of China. With Western sanctions impacting Russia, developments between the EAEU and ASEAN are of significance because there is pent-up demand in Russia for produce – sanctions have halted much of Russia’s natural trade with the EU, for example, and they need to source from elsewhere. ASEAN is a logical move, and one that has already proven success with Vietnam’s trade and investment from Russia significantly increasing following their agreement of an FTA with the EAEU three years ago. The EAEU can also possibly offer a future gateway to Europe for South-East Asian goods.

In terms of basic statistics we can compare ASEAN and the EAEU as follows:

| Bloc | Population (millions) | Land Mass (sqkm) | GDP (US$, PPP) | GDP per capita (US$, PPP) |

|---|---|---|---|---|

| ASEAN | 651 | 4,522,518 | 3 Trillion | 4,600 |

| EAEU | 183 | 20,229,248 | 5 Trillion | 27,000 |

The demographics are of note to ASEAN based manufacturers as the EAEU bloc has a significantly higher GDP per capita income than ASEAN itself – meaning the EAEU market has plenty of money to buy. As I mentioned, due to Western sanctions, it also has plenty of pent-up demand.

The EAEU also has a FTA agreement with China, although the product specifics are still be worked out. We can expect that to come into play in about the next 12 to 18 months. When that happens, Chinese made goods can be transported to the borders of the EU, duty free.

ASEAN members are familiar with the implications having signed off an FTA with China several years ago. Other ASEAN members are already negotiating FTA with the EAEU, most notably Singapore, Indonesia, Cambodia and Thailand, while Malaysia and the Philippines have expressed interest and are studying the matter. India is another country, close to ASEAN, that is also negotiating an FTA with the EAEU. ASEAN itself is also studying the potential for an ASEAN-EAEU FTA.

Clearly, changes and opportunities are coming down the pipeline. When these various FTAs are signed off with the EAEU, the common area of the ASEAN and EAEU nations will change significantly in terms of the development of new supply chains, product availability, the movement of people, and the overall economic development of the two blocs.

Russia, while the principal member of the EAEU, is also a dialogue partner with ASEAN, giving it a seat at the table and therefore able to understand the mechanisms and dynamics of Southeast Asia. Russia actively participates in ASEAN-led multilateral mechanisms, including the East Asia Summit, and the ASEAN Regional Forum amongst others.

Meanwhile, ASEAN and the Eurasian Economic Commission, the main body of the EAEU, have signed off an MoU on Economic Cooperation in November last year. That document can be downloaded here and details customs procedures, e-commerce, technical regulations, trade, investment and finance, and assistance for micro-businesses and SMEs. ASEAN itself is also considering the possibility of a full FTA with the EAEU, an ASEAN-EAEU FTA proposal is currently being studied.

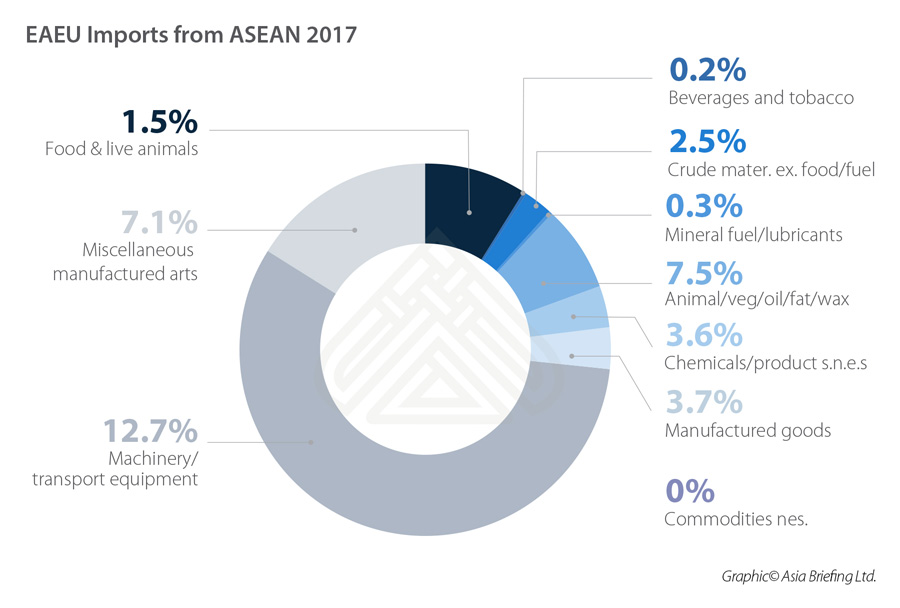

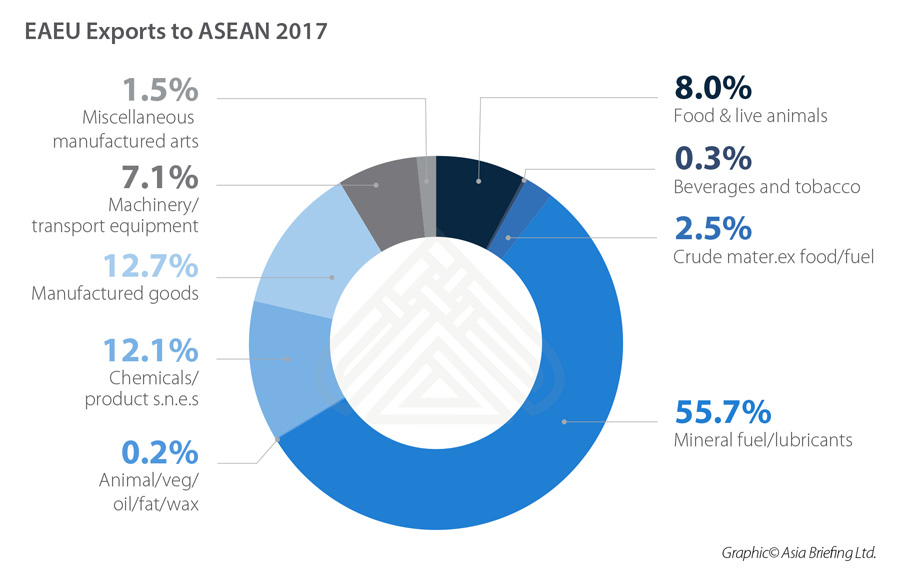

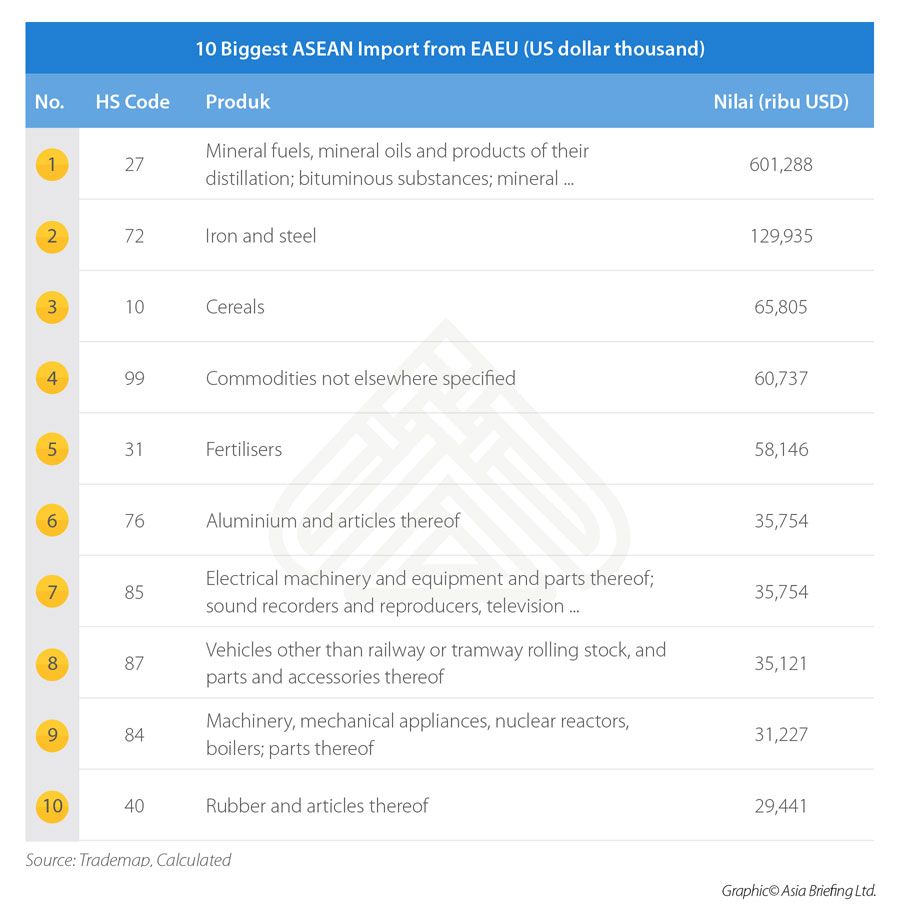

These efforts are having some effect, as we can see in the graphs below.

In terms of traded commodities, we can examine these as follows:

Clearly the scope for trade is wide-ranging, with many items exported from ASEAN to EAEU markets, including Russia.

In terms of FDI, this has been relatively small, with principally EAEU members Kazakhstan and Russia contributing collectively about US$15.4 billion, mainly in the oil, gas and tourism sectors. In return, it is ASEAN members Malaysia, Singapore, Thailand, and Vietnam that have invested the most in the EAEU, about US$9.3 billion, mainly in agriculture, food and tobacco. There are some highlights though – Vietnam is currently the only ASEAN member that has a full FTA with the EAEU; that experience, now entering its third year, has seen mainly Russian investment enter Vietnam, and is now at about US$10 billion. Thailand is also a beneficiary of Russian money as it continues to attract increasing numbers of Russian tourists. Some of these are investing in property and small businesses in the country, a recent phenomena that exists elsewhere across Southeast Asia, including regions such as Goa in India and Sri Lanka. That trend will spread further throughout ASEAN. Businesses in ASEAN countries could do a lot worse than to look out for Russian investors. Sanctions checks to ensure companies are not blacklisted can be carried out by our firm.

There remain significant issues, including matters concerning standards and compliance. However, ASEAN is far more trade influenced – it wants to do business and cut the politics to do business and there is also less pressure exerted from Washington DC on the region. While there are bureaucratic bridges to cross, and negotiations concerning trade to be completed, the emergence of an ASEAN and EAEU trade alliance should not be taken lightly. Processes are underway to line up the trade protocols first to allow an expansion of intra-bloc commerce. As mentioned, with China a significant presence in both, this will provide opportunities for the development of new supply chains. That will impact upon companies currently operating in ASEAN and Russia who may wish, for cost, opportunity, or sanctions reasons, to establish secondary operations elsewhere.

Of the countries involved, for ASEAN members, Russia itself is well worth a look in terms of access to a wealthy and easily defined consumer market, while Belarus offers access to Eastern Europe and potentially the EU, and Armenia the entire Caucasus region. Kazakhstan may be an oil and gas play but it too, has a growing consumer middle class and is Asian in nature, as is Eastern Russia.

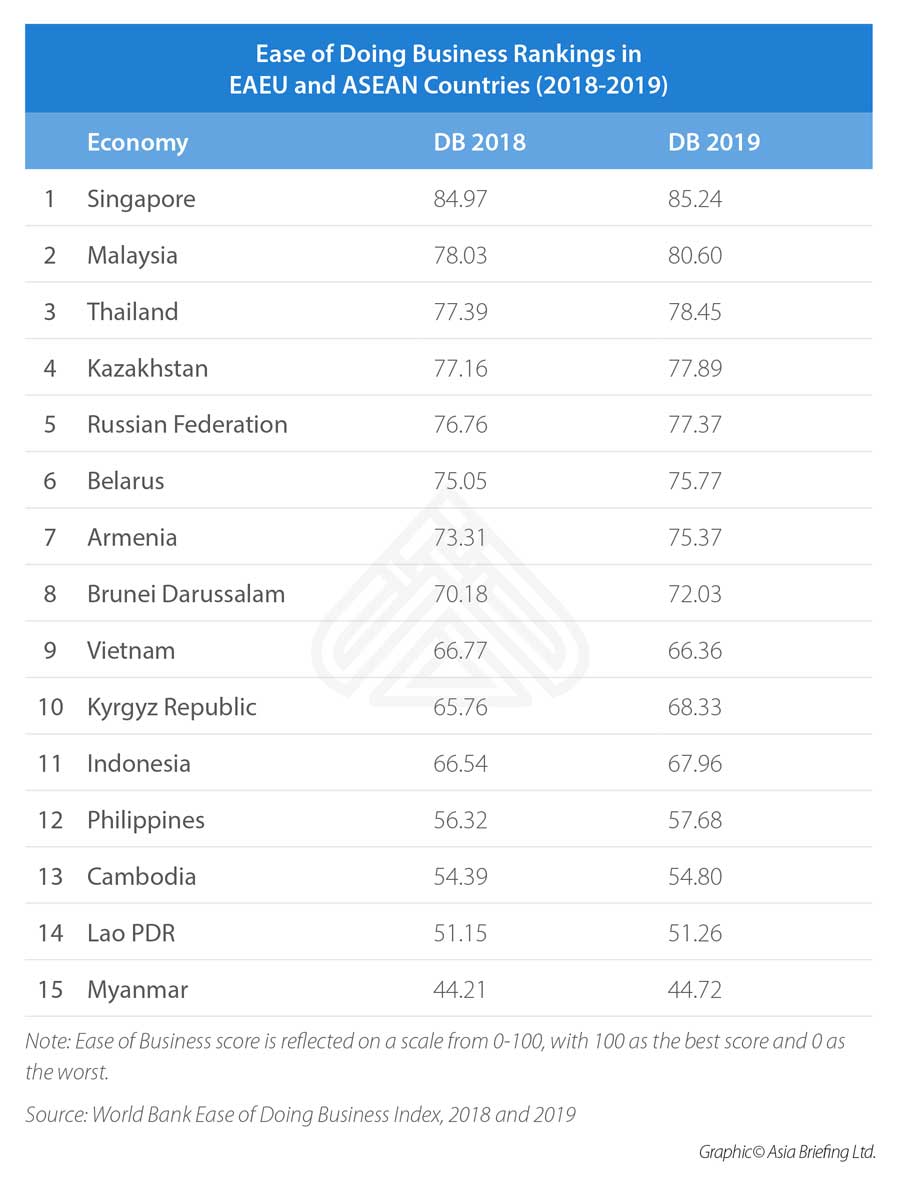

For Russian and other EAEU members, the ASEAN markets of Vietnam, Indonesia, and the Philippines are the best bets at present, with Singapore as a regional financial and services hub. These countries also show up well in the global Ease of Doing Business Rankings, as follows:

In short, at first glance, an alliance between the EAEU and ASEAN doesn’t have an obvious impact. But that is because it hasn’t largely been considered before, these countries seem a long way away. However, the mutual trade in goods is relatively well-balanced and complimentary, while the reach of infrastructure being built as a result of the Belt & Road Initiative impacts positively upon both. While a lot still remains to be done; for foreign investors in Asia, the emerging supply chain potential to and from ASEAN into the EAEU, and elsewhere into China and India, and all the permutations of that need examining. There are costs to be saved and money to be made in doing so, and being the first on the scene. Is your ASEAN business and supply chain potential as concerns the EAEU and Russia on your “to do” list? Because there is money to be made in examining and acting upon the changes that this alliance will bring – and it is happening now.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City and Jakarta. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

![]() Related Reading:

Related Reading:

![]() EAEU & ASEAN Deepen Trade, Economic and Investment Cooperation

EAEU & ASEAN Deepen Trade, Economic and Investment Cooperation

![]() Eurasian Economic Union to Sign Free Trade Deals with Egypt, Iran, India and Singapore

Eurasian Economic Union to Sign Free Trade Deals with Egypt, Iran, India and Singapore

![]() Russian Businesses Expand into Vietnam, ASEAN via the Eurasian Economic Union

Russian Businesses Expand into Vietnam, ASEAN via the Eurasian Economic Union