Singapore Exchange Becomes the First Major Bourse in Asia to Allow SPAC Listings

As of September 3, 2021, the Singapore Exchange (SGX) is among Asia’s first major bourse to allow the listing of special purpose acquisition companies (SPACs) in a move that the city-state hopes will attract more firms to raise funds amid a stagnating initial public offering (IPO) market.

The SGX has introduced a new framework to enable SPACs to list on the exchange, such as minimum market capitalization requirements, minimum SPAC IPO price, and minimum public float, among others.

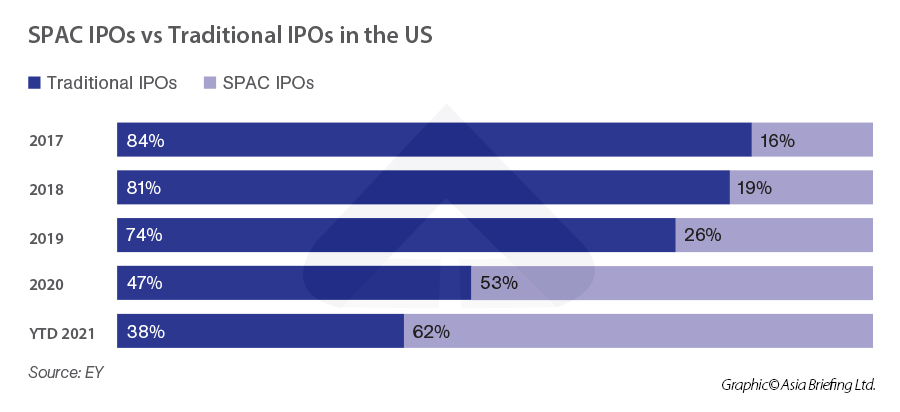

Singapore’s benchmark index has traditionally been dominated by companies in property and finance, but through SPACs, the SGX has set its sights on attracting tech companies.SPACs are essentially shell companies and have no commercial operations. They are formed by investors — who are called sponsors — with the sole purpose of raising money through an IPO to acquire another company, also known as a de-SPAC transaction. The process is often faster than a traditional IPO and has exploded in popularity in the US with 358 SPAC IPOs recorded so far this year; they also account for the majority of global SPAC IPOs (379).

Other advantages with SPACs are their price certainty compared to conventional IPOS and a SPAC transaction allows the target company to negotiate its own fixed valuation with the sponsors.

The SPACs listing framework

The key features of the SPACs listing framework are as follows:

- The minimum market capitalization is S$150 million (US$111 million);

- The de-SPAC must take place within 24 months of IPO with an extension of up to 12 months subject to conditions;

- The minimum SPAC IPO price is S$5 (US$3.7) per share;

- At least 25 percent of the SPAC’s total number of shares issued must be held by at least 300 public shareholders at the time of listing; and

- All independent shareholders are entitled to redemption rights — this mirrors the US SPAC framework.

Assessing suitability

The SGX will also assess a variety of factors when assessing the suitability of a SPAC listing. These include:

- Profile of the founding shareholders and their experience and expertise in managing the SPAC;

- Business strategy of the SPAC;

- Articles of association of the SPAC which provide comparable shareholder protection and rights with that of a Singapore incorporated company; and

- Nature of the compensation of the management team.

Measures related to business combination

As the proceeds raised for SPAC is for the sole purpose of undertaking a business combination (there are several requirements put in place to ensure this is in accordance with this objective:

Holding the IPO proceeds in an escrow account

The framework states that at least 90 percent of the gross IPO proceeds must be placed in an escrow account pending the completion of the business combination.

The escrow agent must be an independent institution approved by the Monetary Authority of Singapore (MAS) and the escrow amount cannot be withdrawn except for the purpose of the business combination, the liquidation of the SPAC, or other specified circumstances.

Allowed timeframe of the completion of the business combination

The SPAC must complete the business combination within 24 months from the date of its listing with an extension of up to 12 months.

If the SPAC has not signed a binding agreement by the end of the 24-month period, the SPAC can seek an extension from the SGX but with a justification as to why they require the extension. The extension must also be approved by at least 75 percent of the votes of shareholders of the SPAC (excluding the votes of the founding shareholders and the management team).The business combination must result in a sizeable new business

The initial business or asset acquired (that is, de-SPAC) must have a market value of at least 80 percent of the amount held in the escrow fund. However, the SGX may be prepared to waiver the 80 percent threshold on a case-by-case basis.

Appointment of a financial adviser

The financial advisor’s role is similar to that of an issue manager in a conventional IPO, and so they must be accredited by the SGX.

Shareholders’ circular must be fully disclosed

The shareholders’ circular must contain prospectus-level disclosures on key areas such as:

- Financial position;

- Compliance history;

- The integrity of incoming directors;

- Permits and approvals; and

- The resolution for the mitigation of the conflict of interests.

This is to ensure that shareholders of the SPAC are making informed decisions when approving a business combination.

SPAC liquidation

The SPAC will be liquidated if the business combination is not complete within the timeframe or there is a material change to the founding shareholders or management. Upon liquidation, the remaining funds in the escrow accounts will be distributed on a pro-rata basis to all shareholders.

Aligning the interests of the founding shareholders with independent shareholders

The SPAC framework hopes to ensure the interests of the founding shareholders are aligned with the independent shareholders by subjecting the founding shareholders and management to a percentage-based minimum equity participation (MEP) requirement. The MEP is between 2.5 to 3 percent at IPO, depending on the SPAC market capitalization.

Moreover, moratoriums will apply similarly to an issuer listed on the SGX via a traditional IPO. Thus, a moratorium will be observed for the founding shareholders and management team of the SPAC, the controlling shareholders of the resulting issuer, and their associates.

Supporting Singapore’s stagnant IPO market

The introduction of the SPAC framework can provide much-needed enthusiasm to Singapore’s IPO market, which has not drawn much interest from domestic and international businesses this year.

Singapore only saw three listings in the first half of 2021 – a 50 percent decrease from 2020 – whereas Hong Kong – considered a rival financial hub – saw 46 listings during the same period.

These three IPOs raised some US$250 million in proceeds while Hong Kong’s 46 IPOs raised US$27.4 billion. As such, the government hopes the initiatives introduced under the SPAC framework will bring more tech companies to list on the SGX and give the SGX a competitive advantage over regional rivals, particularly since a company needs a valuation of at least US$5 billion to attract investors interest in the US stock market. The SGX could be another option for tech companies with smaller valuations.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City, and Da Nang in Vietnam, Munich, and Esen in Germany, Boston, and Salt Lake City in the United States, Milan, Conegliano, and Udine in Italy, in addition to Jakarta, and Batam in Indonesia. We also have partner firms in Malaysia, Bangladesh, the Philippines, and Thailand as well as our practices in China and India. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Indonesia’s Omnibus Law: Changes to the Immigration Law

- Next Article The US-ASEAN Trade and Investment Facilitation Agreement Explained